Running a business is exhilarating. You set your own hours, build something you’re proud of, and answer to nobody but your clients (and occasionally your accountant). But here’s the part nobody tells you at the grand opening: retirement planning for small business owners is entirely on you. No HR department is auto-enrolling you in anything. No employer is quietly matching your contributions. It’s just you, your income, and the decisions you make today.

The good news? The self-employed retirement accounts available to you are genuinely powerful and the tax deductions that come with them are, frankly, spectacular. This guide will walk you through your options clearly so you can stop putting this off and actually build the retirement you deserve.

As a small business owner, your best retirement savings vehicles are the SEP IRA, Solo 401(k), and SIMPLE IRA. Each has different contribution limits, setup rules, and tax advantages. For 2025, you can potentially stash up to $70,000 (or more with catch-up contributions) into a retirement account and deduct most or all of it. Your choice of plan comes down to your business structure, income, and whether you have employees.

Why Retirement Planning Hits Differently When You’re Self-Employed

Think of it this way: a salaried employee at a big company is like a passenger on a cruise ship: meals scheduled, entertainment planned, retirement contributions automatic. You, the small business owner, are the captain of your own vessel. You decide the destination, the speed, and yes, whether anyone thought to pack enough fuel for the long haul.

Running a small business means balancing a lot of financial priorities, but retirement planning should never fall by the wayside. Without employer-sponsored plans, you need to take action to secure your future.

The right plan isn’t only about saving, it can offer significant tax benefits. Contributions are generally tax-deductible for the business, and investment earnings grow tax-deferred (or tax-free with Roth contributions).

That’s a double win: you save on taxes now and grow your money for later.

Your Main Owner Retirement Savings Options

There are three self-employed retirement accounts that do the heavy lifting for most small business owners. Let’s break them down honestly.

SEP IRA: The Elegant Simplicity Option

SEP IRA: The Elegant Simplicity Option

The SEP IRA, or Simplified Employee Pension, is where many solo entrepreneurs start, and for good reason.

It is easy to set up, requires minimal ongoing paperwork, and works for solo business owners or small businesses with employees.

For 2025, the SEP IRA contribution limit is 25% of an employee’s total compensation, up to $70,000. If you are self-employed, your contributions are generally limited to 20% of your net income because of how the IRS calculates self-employment earnings.

The SEP’s biggest advantage is timing. It can generally be established as late as the due date of the employer’s tax return, including extensions. That makes it useful if you are doing taxes in March and realize you need a deduction.

The catch is that SEP IRAs do not allow employee salary deferrals. They only allow employer contributions, made at the employer’s discretion. If you have staff, most SEP plans require you to contribute the same percentage of pay for each eligible employee.

Solo 401(k): The Power Move for Owner-Only Businesses

If you run an owner-only business, this is the plan worth getting excited about.

A solo 401(k), which the IRS calls a one-participant 401(k), is usually the most versatile option for a business owner with no employees other than a spouse.

As the business owner, you can contribute as both employee and employer. For 2025, you can defer up to $23,500 in salary, plus a $7,500 catch-up contribution for ages 50–59.

Employer profit-sharing contributions can bring total solo 401(k) contributions to $70,000. For ages 60–63, the higher catch-up can bring the total to $81,250.

Both Roth and traditional options are available, and loans may be permitted. Once plan assets exceed $250,000, annual Form 5500-EZ filing is required.

SIMPLE IRA: The Best Friend of Small Teams

If you have employees and want an easy way to offer them a meaningful benefit, the SIMPLE IRA earns its name.

A SIMPLE IRA is designed for smaller employers that want an employee retirement plan without the complexity of a conventional 401(k).

For 2025, the maximum employee salary deferral is $16,500, with a catch-up contribution for ages 50–59 of $3,500, for a total of $20,000.

But here’s the non-negotiable part:nthe employer contribution is not optional. The employer generally must either make a matching contribution or a nonelective contribution, subject to the SIMPLE rules.

Also worth flagging: early withdrawals within the first two years are subject to a 25% penalty greater than the usual 10%.

So this plan rewards commitment.

SEP IRA vs Solo 401(k): The Head-to-Head

This is the comparison most self-employed owners are really asking about. Both plans share the same $70,000 ceiling for 2025, but how you *get* It is very different.

Self-employed people may be able to save more in a solo 401(k) than they can in a SEP IRA. Solo 401(k)s let you make both employee and employer contributions, meaning you can contribute up to $23,500 for 2025 as an employee, even if that is 100% of your self-employed earnings for the year, and you can also contribute 20% of your net self-employment income.

In plain English: if your income is modest, say, $50,000 a Solo 401(k) lets you sock away far more because of the employee deferral component. A SEP IRA at the same income level caps you at roughly $10,000. That gap matters enormously early in your business journey.

SEP IRAs offer simplicity and late funding flexibility, but they rely on employer contributions and can become expensive once employees are eligible.

The Solo 401(k), on the other hand, often creates the strongest savings opportunity for an owner-only business, but it introduces more administration and is only available while the business remains effectively owner-and-spouse only.

Bottom line?

For business owners, the retirement-plan question is rarely just which option allows the biggest contribution. The more useful question is which plan best fits your income pattern, headcount, tax posture, and tolerance for administration.

Retirement Tax Deduction Strategies Worth Knowing

The tax upside here is real and often underused.

Contributions to a SEP IRA up to the annual limit are tax-deductible for the employer and aren’t subject to federal income tax for the employee until distributions are made. Self-employed individuals can typically deduct the entirety of their allowable SEP IRA contributions.

A few smart moves to layer on top:

Stack a Roth IRA alongside your business plan.

A Roth or traditional IRA can offer additional tax-advantaged ways to save beyond a self-employed or small business plan.

For 2025, the maximum contribution to all IRAs combined is $7,000 if under age 50, or $8,000 if age 50 or older.

Think about future tax brackets.

Roth contribution options are available for both employers and employees. Pre-tax distributions are taxed upon withdrawal, while Roth contribution portions are made with post-tax dollars, and distributions in retirement are not taxable.

If you expect to be in a higher tax bracket later, Roth wins. If you need the deduction now, traditional wins.

Don’t sleep on the spousal opportunity.

A spouse can be added to a solo 401(k) plan whether they act as a W-2 employee or an owner in the business which effectively doubles your solo 401(k) contribution limits for your household.

How to Choose the Right Plan for Your Business

Still not sure which self-employed retirement account fits your situation? Here’s a fast framework:

For owner-only businesses focused on maximizing retirement savings efficiently, the solo 401(k) is often the first plan worth evaluating.

Businesses with employees may want to consider a SIMPLE IRA, especially when they need a relatively manageable benefit.

A SEP IRA can also be compelling for owners who value ease and the ability to decide late, as long as the employee cost is acceptable.

And remember these plans aren’t necessarily mutually exclusive forever. As your business grows and evolves, your plan can evolve too. Starting with a SEP IRA in year one doesn’t mean staying there in year five.

FAQ: Retirement Planning for Small Business Owners

Can I have both a SEP IRA and a Solo 401(k) at the same time?

It is possible to have both a SEP IRA and a solo 401(k). However, how much you can contribute to them depends on certain factors, including how your SEP was set up. In general, when you contribute to both plans at the same time, there is a limit to how much you can contribute. Your total contributions to both are aggregated and cannot exceed $70,000 in 2025.

What’s the deadline to set up and fund these accounts?

You have until April 15 (plus extensions) to establish a SEP IRA for the current tax-reporting year.

For a Solo 401(k), the deadline for self-employed individuals and owner-only businesses to make both the employee salary deferral and company profit-sharing contribution is the business’s tax filing deadline, including extensions.

Note that the plan itself typically must be established by December 31 of the tax year.

What if my income is inconsistent is there a flexible option?

A SEP IRA is a great option for solo entrepreneurs or small businesses with variable profits who want maximum flexibility.

Since contributions aren’t required every year, you can contribute a lot in a strong year and nothing in a lean one, no penalties, no drama.

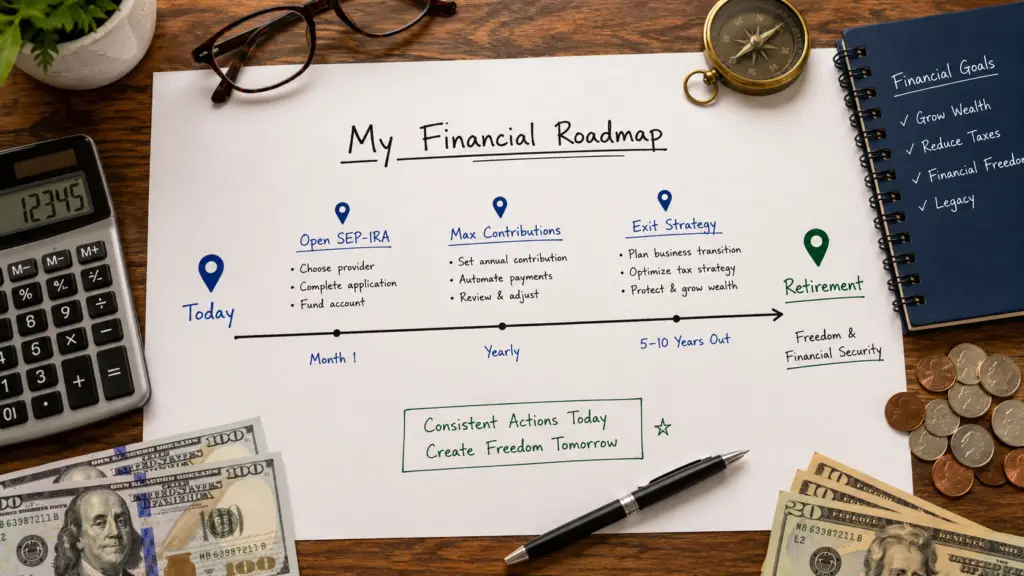

Start Now, Thank Yourself Later

There’s no perfect moment to start retirement planning for small business owners. The perfect moment was five years ago. The second-best moment is today. Whether you open a SEP IRA this weekend or spend the next few weeks comparing a Solo 401(k) with your accountant, the point is to *move*.

Your business is already proof that you can build something meaningful from scratch. Your retirement savings can be the same story. Pick a plan, open an account, and make your future self very, very happy.

Ready to take the next step? Talk to a fee-only financial advisor or CPA who specializes in self-employed clients. They can help you run the numbers and choose the plan that fits your specific business and tax situation.

*Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Consult a qualified professional before making retirement planning decisions.*