Most people treat taxes like a dentist appointment, something to dread, delay, and get through as fast as possible. You show up in April, hand over your documents, wince at the number, and move on. But here’s the uncomfortable truth: if you’re only thinking about taxes once a year, you’re almost certainly leaving real money on the table. A proactive tax planning strategy changes that entirely. It’s not about scrambling before the deadline. It’s about making smarter decisions all year long so the deadline is basically a formality.

Tax preparation files what already happened. A proactive tax planning strategy shapes what’s about to happen and that difference can cost (or save) you thousands every single year.

What Is Tax Preparation, Really?

Tax preparation is the annual process of filing your tax return with the IRS. The goal is to file correctly in order to avoid penalties.

That’s it. It’s a look in the rearview mirror.

Tax preparation primarily focuses on your past financial activity instead of any type of future strategy.

Your tax preparer is working with decisions you already made: the salary you earned, the investments you sold, the deductions you either captured or missed.

During tax preparation, you can maximize all available credits and deductions. But you are bound by taking advantage of what is available, rather than proactively creating new savings opportunities.

Think of it like reviewing game film after you’ve already lost the match. Useful? Sure. But it won’t change the score.

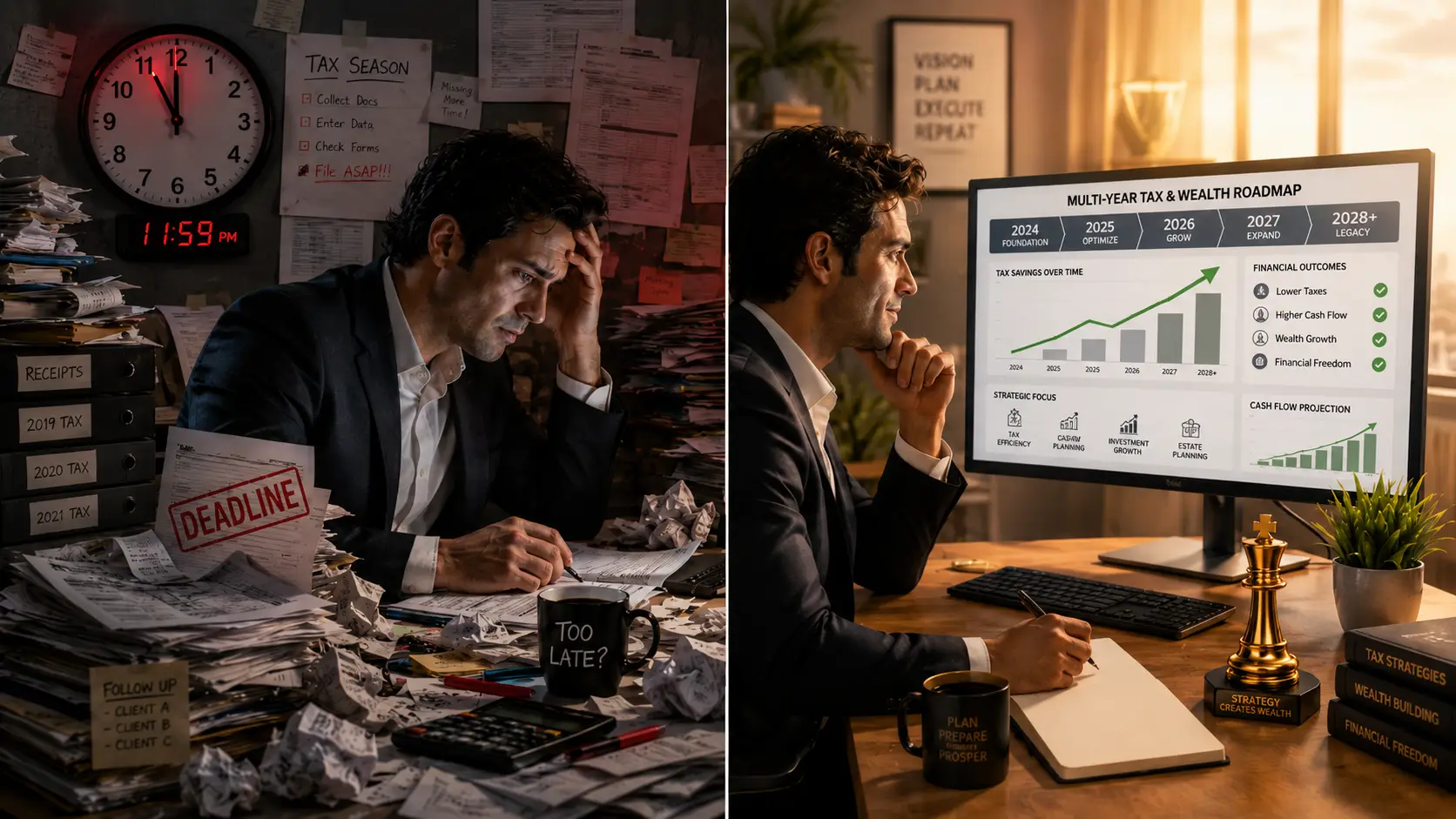

Many taxpayers fall into the trap of reactive tax planning. They scramble to gather documents and make last-minute decisions as the tax deadline approaches. This method often results in missed opportunities and higher tax bills.

So What Is a Proactive Tax Planning Strategy?

Tax planning is the analysis and arrangement of a person’s financial situation to maximize tax breaks and minimize tax liabilities legally and efficiently.

But what really separates it from preparation is the timing and the mindset.

Tax preparation records your history, while tax strategy shapes your future.

A proactive tax planning strategy means you’re having conversations with your advisor in July and October, not just April. You’re making financial moves with intention before the year closes and the options disappear.

Traditional tax prep happens after the fact once the year has ended and the options are gone. It’s like trying to fix your swing after you’ve already missed the ball.

Tax planning is a proactive and ongoing process. It takes into consideration the changing tax landscape as you move through life stages such as marriage, children, and retirement.

That last part matters. Your tax situation isn’t static. Neither should your strategy be.

The Real Cost of Waiting Until April

Here’s a concrete example that hits home.

For people with regular W-2 incomes, a purely reactive approach works just fine but for high earners, business owners, and real estate investors, it’s often not the best approach.

As your revenue increases, so does your tax complexity. A deduction you overlooked at $500,000 in revenue could cost you tens of thousands at $5 million.

And it’s not just business owners.

A proactive approach to tax planning unlocks a wide variety of benefits, but ultimately they all add up to one key concept: you get to keep more of your hard-earned money. In the short term, proactive tax planning enables you to take advantage of all the opportunities available to you, and can help you save tens of thousands of dollars from Year 1.

The difference isn’t theoretical; it’s dollars you either keep or hand over to the IRS.

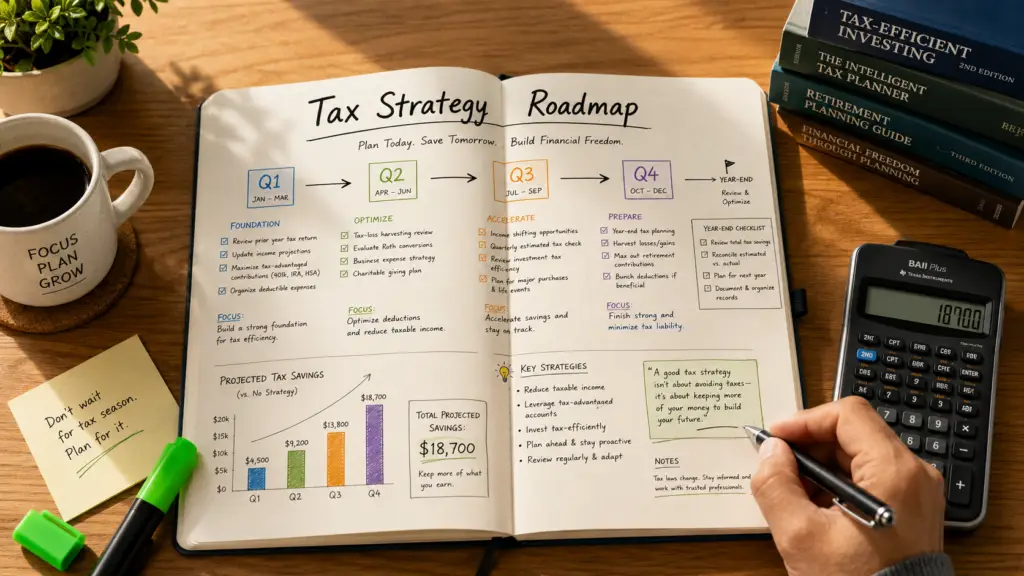

A Year-Round Tax Strategy: What It Actually Looks Like

The phrase “year-round tax strategy” sounds exhausting. It’s not. It’s mostly about being intentional at the right moments throughout the year, rather than panicking in one. Here’s what forward-looking tax advice and reduction planning actually involve in practice.

Timing Your Income and Deductions Strategically

Timing income can reduce your tax bill. Deferring income or pushing deductions into a different year may help, while sometimes recognizing income sooner makes sense especially if you anticipate a higher rate next year.

This kind of decision can’t be made in April. It has to happen before December 31.

If you’re close to the next tax bracket, consider deferring income like a year-end bonus to the following year to keep your current tax bill lower.

That’s a one-sentence strategy that could save you a meaningful amount, but only if someone’s watching it proactively.

Maximizing Tax-Advantaged Accounts to Minimize Tax Liability Legally

Utilizing tax-advantaged investment vehicles forms a critical component of proactive tax planning. Accounts such as 401(k)s, IRAs, and Health Savings Accounts offer significant tax benefits that can reduce current tax liability and help build long-term wealth.

For 2025, the contribution limit for 401(k) plans stands at $23,500, up from $23,000 in 2024. Maximizing these contributions can significantly reduce taxable income.

And don’t overlook HSAs.

Health Savings Accounts provide triple tax benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

That’s a genuinely rare hat trick in the tax code.

Tax-Loss Harvesting Throughout the Year

When rebalancing your portfolio, you may be able to reduce your tax liability by offsetting any realized capital gains with your losses. Tally up your gains, then sell less attractive, losing positions of equal value. If you have more losses than gains, you can offset up to $3,000 of ordinary income.

This isn’t something you can set up retroactively. It requires monitoring your portfolio with tax awareness in mind all year long.

Strategic Charitable Giving

If you’re philanthropically minded, you may be interested in incorporating charitable giving into your financial plan. Considering you may only deduct charitable contributions if you’re itemizing deductions, it takes some proactive planning to ensure you optimize your donations’ tax impact.

High earners can fund charitable lead trusts, donor-advised funds, or retirement accounts in ways that reduce today’s tax bill and support long-term goals.

Giving generously and keeping more of what you earn aren’t mutually exclusive but only if you plan.

How Tax Law Changes Make Proactive Planning Even More Critical

Tax law isn’t static. What worked two years ago might not work next year.

This is especially true right now.

As the landscape of tax legislation evolves, taxpayers find themselves navigating a complex and ever-changing environment. Each investor’s financial situation is unique, influenced by factors such as income, investments, and family circumstances, making personalized tax planning more crucial than ever.

Amidst the uncertainty, there are certain proactive strategies that can benefit taxpayers regardless of the specific legislative changes that may come.

That’s the whole point of a forward-looking tax approach: you’re not reacting to new laws after they hit. You’re already positioned.

FAQ: Proactive Tax Planning Strategy

Is tax planning only for wealthy people or business owners?

Not at all.

Tax planning is a proactive financial practice that helps individuals and businesses manage their taxes and make smart financial decisions. This approach involves continuous monitoring and adjustment of financial decisions to optimize tax outcomes.

Whether you’re a freelancer, a salaried employee with investments, or a small business owner, there are strategies that apply to you.

Can’t my tax preparer just handle this at filing time?

Tax planning involves making financial decisions throughout the year to reduce your tax burden. Preparation is compiling documents and filing returns by then, most opportunities have passed.

A great preparer files your return accurately. But they can’t undo financial decisions you made eleven months ago.

How much can a proactive tax planning strategy actually save me?

It depends on your situation, but the potential is real.

By proactively analyzing income, expenses, investments, and potential deductions, tax planning minimizes tax liabilities and maximizes after-tax income. Effective tax planning also ensures cash flow stability and mitigates the risk of penalties.

The more complex your finances, the more a year-round strategy tends to pay for itself often many times over.

Stop Filing. Start Planning.

There is no such thing as “tax season.” Now is the time to get a head start on your taxes so your money can work harder, last longer, and serve you better.

A proactive tax planning strategy isn’t a luxury for the ultra-rich. It’s a smarter, calmer, more financially sound way to manage one of your biggest annual expenses.

Shifting from a once-a-year focus to a continuous process helps you better preserve and grow your wealth.

And honestly, that peace of mind alone is worth something.

Proactive tax planning reduces the stress associated with tax season. It ensures consistent compliance with tax laws, which is important considering the potential penalties for non-compliance. Staying ahead of your tax obligations helps you avoid the rush and potential errors that come with last-minute filing.

Ready to stop reacting and start planning? Schedule a consultation with me today about building a year-round tax strategy that’s tailored to your financial picture. The best time to start was last January. The second best time is right now.

*Disclaimer: This article is for informational and educational purposes only and does not constitute tax or legal advice. Please consult a qualified tax professional for guidance specific to your situation.*